RESOURCE CENTER

Medicare Insights & Expert Advice

Many people find the Annual Enrollment Period quite confusing, so we created an easy-to-follow checklist to help guide you through it. Things to know about the Annual Enrollment Period When is the Medicare Annual Enrollment Period? It is a period that runs from October 15th to December 7th each year. It is important to keep in mind your Medicare Supplement (Medigap) policy will not be affected during this time. Medigap benefits remain the same each year. However, you can shop rates if you're looking for lower premiums. Medicare Advantage plans (Part C) and Prescription Drug Plans (Part D) DO change. These plans must renew their contracts with Medicare annually, which allows them to change premiums, co-pays, networks and drug formularies. Therefore, it is essential to review and understand any upcoming changes to your plan. The Annual Enrollment Period (AEP) is your opportunity to decide whether to keep your current plan or switch to a new one. 5 Steps to take during the Annual Enrollment Period 1. Review your annual notice of change letter Your plan is required to send you an Annual Notice of Change packet by the end of September. Take the time to review any upcoming changes to your plan and decide if you want to explore new options for more benefits or lower premiums. If you are satisfied with your current plan, no action is needed. It will automatically renew on January 1st. 2. Compare your prescription drug costs Your plan may change the costs of your prescription medications each year. It is recommended to review your Annual Notice of Change letter to ensure that all of your out-of-pocket drug costs remain affordable. 3. Verify that your doctors are in network Medicare Advantage (Part C) plans have networks. Each plan offers a directory of network providers you can search to see who participates in the plan’s network. Doctors can leave a Medicare Advantage plan network at any time. Even if you aren't changing plans, make sure to check that your doctors are still in network with your current plan. 4. Decide if your plan still meet your healthcare needs Medicare health plans can introduce new benefits and services each year. These benefits may include dental, vision, hearing, fitness memberships, transportation services, among other programs that can help you save on your Medicare premium. Most importantly, comparing these new offerings can help you find the coverage that’s most suitable for your needs. Last but not least - Don’t miss the deadline 5. Schedule a No-Cost Annual Medicare Review Now that you know how the Medicare Annual Enrollment Period (AEP) works, it is time to schedule a date on your calendar to review your choices. Our team at Seniors Health can help you weigh your options, so you can make an informed decision. Representing dozens of top-rated carriers, we can help you compare plans, run quotes and find the most cost-effective plan in your area. Best of all - Our service is free and our team is here to ensure that you are getting the most out of your Medicare coverage. Please do not hesitate to reach out. You can call Monday through Friday - anytime from 9:00 am to 5:00 pm at 855-278-2700. We hope you found this information helpful and we look forward to assisting you. Have questions? Contact a Seniors Health agent today and let us know how we can help.

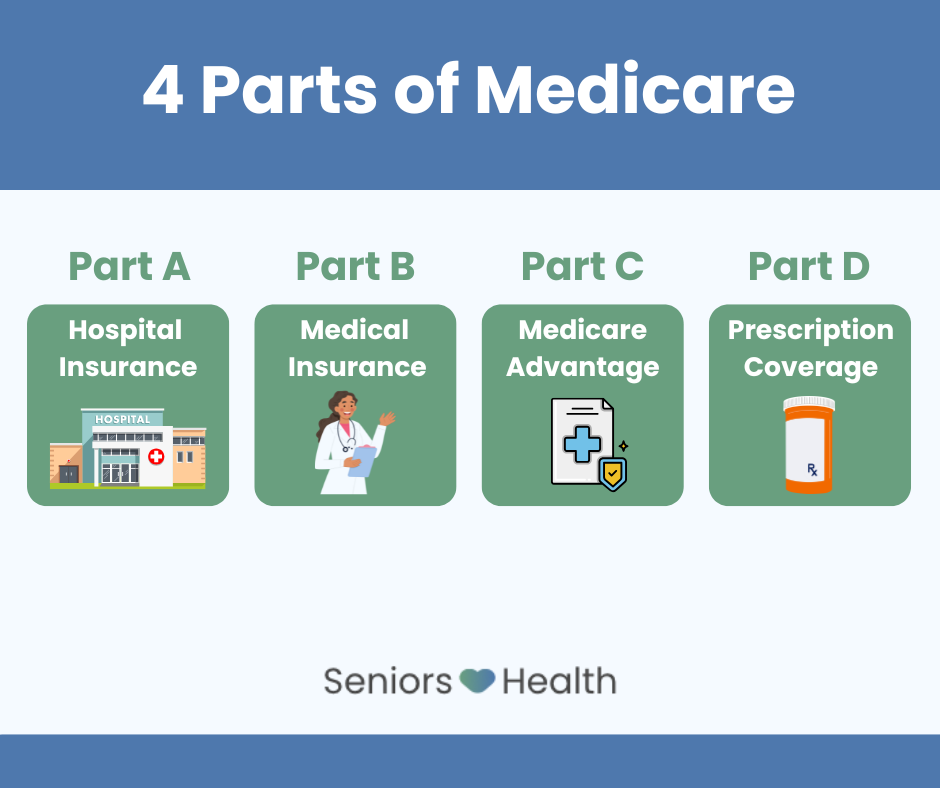

Medicare is the federal health insurance program for people 65 and over, some younger with disabilities and those with End Stage Renal Disease. Medicare is a different program from Medicaid, which offers healthcare and services to those who meet the qualified lower income requirements. Anyone receiving Social Security Disability (SSDI) for 24 months, will also become eligible for Medicare. When discussing some of the Medicare basics, It’s important to know that there are 4 Parts of Medicare and each part works in a unique way to help cover your healthcare expenses. What Is Medicare Part A and What Does It Cover? Medicare Part A is inpatient and hospital insurance. Part A helps cover: Inpatient hospital care Skilled nursing facility care Hospice care Some home health care What is Medicare Part B and What Does It Cover? Medicare Part B is outpatient medical insurance. Part B helps cover: Services from a doctor Outpatient care Durable medical equipment Preventative services Some home health care What Is Medicare Part C? Medicare Part C (Medicare Advantage) are privately managed, federally approved Medicare plans. Part C plans combine the benefits of Part A and B into one plan and may also include: Prescription drug coverage Dental, vision and hearing coverage Wellness programs and telehealth services What Is Medicare Part D? Medicare Part D plans provide beneficiaries with privately managed, federally approved prescription drug coverage. Medicare Part A and B do not offer prescription drug coverage, so Part D helps: Manage prescription drug costs Provide lower cost-sharing for in-network and preferred pharmacies What does Medicare Pay? Medicare generally covers 80% of your Part A and Part B medical costs. You are responsible for the remaining 20%. There is no limit on what you pay out of pocket, unless you have Medicare Supplement coverage, also known as Medigap. You could also choose to get your coverage through a Medicare Advantage plan, also known as Part C. It is important to understand how each of these coverages work, when making a decision on how you would like to receive your benefits. New to Medicare with Employer Coverage? You should consider whether it makes sense to keep your employer coverage alongside Medicare or if switching to Medicare as your primary insurance would be a better option. A few key questions would include: How large or small is the employer? How much is your monthly premium? Would you like to have more freedom to choose any provider that accepts Medicare? When it comes to Medicare, there is no one size fits all. Knowing your situation and what you find important, provides answers that help determine which road may be more suitable for you. Avoid Costly Medicare Mistakes - Get Expert Advice We understand that learning about Medicare can seem confusing. Especially knowing when and how to sign up for each part, to ensure you don’t miss any important deadlines. This is where our team of friendly agents can help. To learn which coverage options best suit your needs and how to avoid unexpected medical costs, contact us for a no-cost personalized review.

When is the Initial Enrollment Period? (IEP) The Initial Enrollment Period begins 3 months before your 65th birthday month, the month of and 3 months after. The Initial enrollment period is a 7-month window where you enroll into Medicare for the first time. You can choose to enroll in Medicare Part A and/or Part B. You may also be eligible to enroll into a Medicare Advantage Plan or Part D Drug Plan. What if I missed my Initial Medicare Enrollment Period? Missing your initial enrollment period could negatively impact you financially. By not enrolling on time, you may incur a late enrollment penalty. This penalty amount can increase over time or for as long as you are not receiving coverage. If you missed your Initial Enrollment Period, you would have to wait until the General Enrollment Period to be eligible to enroll. When is the Medicare Annual Enrollment Period? (AEP) Medicare’s Annual Enrollment Period begins on October 15th and ends on December 7th. During this time, Medicare beneficiaries can enroll, change or dis-enroll from a Medicare Advantage Plan or Part D (Prescription Drug Plan). If you were not able to enroll in a Medicare plan during your Initial Enrollment Period, this would be your opportunity to explore your options before you miss the deadline. It’s very important to review your current coverage annually to ensure that your health needs are being met for the following year. Do I need to re-enroll in my Medicare plan every year? Generally, you will be automatically enrolled into your current Medicare plan every year, unless you feel that your Medicare plan no longer meets your budget or specific goals. If you feel that you are missing important benefits such as dental, vision or hearing, then this would be the time of year to compare your options. During this time, you may also find Part D plans that offer lower prescription drug costs. Whether you choose to make changes or not, this is the time to make sure that you are receiving all the benefits being offered in your area and to ask questions (before the December 7th deadline). When is the General Enrollment Period? (GEP) The General Enrollment Period starts on January 1st and ends on March 31st. During this time, you could enroll into Original Medicare, if you missed your Initial Enrollment Period and did not qualify for a Special Enrollment Period. Keep in mind that although you may sign up for Original Medicare, you may be subject to late enrollment penalties. Also, if you would like to enroll into a Medicare Advantage or Medicare Part D (Prescription Drug coverage) during this time, you will have to wait until the Annual Enrollment Period to be eligible. When is the Medicare Advantage Open Enrollment Period? (MA OEP) The Medicare Advantage Open Enrollment Period begins on January 1st and ends on March 31st. This Open Enrollment Period is for beneficiaries who are already enrolled in a Medicare Advantage Plan and want to leave or change to a different Medicare Advantage Plan. Also, you may switch back to Original Medicare with or without Part D drug coverage. However, you will not be able to change from a Part D to another Part D (Prescription Drug) Plan. What is a Special Enrollment Period? (SEP) The Medicare Special Enrollment Period (SEP) is an 8-month period that begins the month you or your spouse retire from work, or the month that your group coverage ends (whichever comes first). If you’ve had health coverage through your employer, you can enroll in Part A and/or Part B, since you’ve had creditable coverage through a group health plan. There are certain circumstances that can make you eligible for a Special Election Period. If you have moved outside of your plan’s service area, you will have two months to make changes to your coverage. When is the Medigap Open Enrollment Period? This period automatically starts the first month you have Medicare Part B and you’re 65 or older. During this 6-month Medigap Open Enrollment Period, those looking to buy a Medigap Policy will generally get better pricing and have more available choices. During this period, you can get a Medigap policy sold in your state, even if you have health problems. After this enrollment period ends, you may not be able to buy a Medigap policy if you are unable to pass a medical underwriting review. Can I change Medigap plans anytime during the year? You may be able to change your Medigap plan during the year, but this depends on your overall health and if you are able to qualify for a new policy. If you haven't compared plans or premiums in a while, doing so could lead to a great opportunity for savings. Get Help with Your Medicare Options We understand that everyone’s situation is unique and it can be a bit overwhelming to make this important decision on your own. This is where we can help. We are experts when it comes to simplifying Medicare and we provide each beneficiary with a no cost Medicare review. This helps us understand your specific health needs, budget and we can help determine what may be the perfect plan for you. Whether you are retired, about to retire, new to Medicare or currently looking at your options, we’d love to help and answer all your questions and help you understand your choices.

Medigap and Medicare Advantage are two different ways to receive your Medicare coverage. What do they have in common and how are they different? Understanding this can help you make a good choice on which is better for your specific situation. What are the differences between Medigap and Medicare Advantage? Medigap Insurance Medicare Supplement coverage, also known as a Medigap plan, is designed to fill the gaps in Original Medicare. These are private insurance policies that help pay for some of the healthcare costs that Original Medicare doesn't cover such as copayments, coinsurance and deductibles. Medicare Advantage Medicare Advantage is a Medicare approved plan from a private company that offers an alternative to Original Medicare. These bundled plans include Part A, Part B and usually offer additional benefits and most include prescription drug coverage. What are the Pros and Cons of Medigap? Pros Medigap plans provide additional coverage, which helps cover costs not paid by Original Medicare. It often provides more predictable out-of-pocket costs due to it's comprehensive coverage. You have more freedom of choice, which allows you to choose any doctor that accepts Medicare without network restrictions. Generally, you can expect consistent coverage and stability, as Medigap policies are standardized. Cons Medigap typically comes with a higher monthly premium. Medigap plans do not include prescription coverage, so you will need to purchase a Part D plan. You cannot use Medigap with Medicare Advantage plans; it's only for Original Medicare. What are the Pros and Cons of Medicare Advantage? Pros Medicare Advantage combines Part A, Part B and often Part D in one plan. Many plans have lower or even $0 monthly premiums. Some plans offer extra benefits like dental, vision, hearing and fitness memberships. Most plans have a maximum limit on out-of-pocket expenses. Cons These plans have networks. You may need to use doctors and hospitals within the plan's network. If you go outside the network, you may face higher out of network costs. Some services may require prior authorization, which is an approval before receiving certain services. Medicare Advantage plans can change their benefits and costs each year. How do I choose between Medigap and Medicare Advantage? When deciding whether to get a Medigap or a Medicare Advantage plan, there are a few things to consider. You can either use original Medicare with a Medigap policy or choose a private Medicare Advantage plan. If you go with Original Medicare, you can see any doctor or facility that accepts Medicare. However, you will need to buy separate policies to help with out of pocket costs. If you choose Medicare Advantage, you may pay low or no premium, besides your monthly Part B premium. Keep in mind that out-of-pocket costs can vary if you use more medical services. Medicare Advantage plans have networks, so you may have to see doctors within their network. Depending on the plan, if you visit an out-of-network doctor, your plan might not cover the visit or you might have to pay more. Also, some services may require prior authorization before the service is covered by the plan. Get help navigating your Medicare options We understand comparing different Medicare plans and deciding on the right one can feel overwhelming, but it doesn't have to be! Our expert team can assist you with your plan options and help ensure your coverage meets your budget and specific needs. We can look through multiple Medicare plans from various insurance carriers and see which may be the right fit for you. Feel free to give us a call today and we will help you compare prices and benefits all in one place.

Original Medicare (Part A & Part B), does not cover regular eye exams or other vision costs, except in certain situations. However, people on Medicare can look into other options. They may get vision coverage through separate insurance or through a Medicare Advantage plan (Part C) that include vision benefits. What does Medicare cover for vision? Medicare covers eye exams to check for specific medical conditions, such as: For those with diabetes Medicare provides coverage for an annual eye examination to screen for diabetic retinopathy, a condition characterized by damage to the eye's blood vessels. Your risk for this condition increases the longer you live with diabetes. This exam must be performed by an eye doctor licensed in your state. For individuals at high risk for glaucoma Medicare offers coverage for an annual glaucoma test if you're considered to be at high risk. High-risk individuals are those with diabetes or those who have a family history of glaucoma. Glaucoma includes a group of eye conditions that cause damage to the optic nerve. For individuals with age-related macular degeneration Medicare offers coverage for specific tests and treatments, including certain drug injections, for age-related macular degeneration, an eye condition that affects a small central part of the retina. Are glasses covered by Medicare? Medicare typically does not cover glasses. However, it may cover certain eye exams and procedures related to medical conditions, such as cataracts. If you require glasses after surgery or a medical treatment, coverage might be available, but this is limited. For routine vision care, like eye exams and glasses, you may need to get a separate vision insurance plan. How can I save money on vision care? To save on vision care, consider these tips: Regular Eye Exams: Visit an eye doctor annually to catch any issues early, which can help prevent costly treatments later. Insurance Benefits: Check your vision insurance for discounts on exams, glasses, or contacts. Use in-network providers for better rates. Use Flexible Spending Accounts (FSAs): If offered by an employer, FSAs can help you save tax-free money for vision expenses. Buy Generic: Opt for generic lenses and frames when possible. They often offer similar quality at a lower price. Consider Vision Plans: If your insurance doesn’t cover vision, explore standalone vision plans that can help reduce costs. Understanding Coverage under Medicare Part C To get coverage for regular eye exams, you may want to consider a Medicare Advantage plan. These plans are run by private insurance companies and offer additional benefits. Many Medicare Advantage plans help pay for glasses, contact lenses and even pay for routine eye exams. If this is important to you, check your plan details. Remember that benefits vary by plan and not all plans are the same in every area. Get Help with Vision Coverage We know the importance of maintaining good eye health during your golden years. However, Medicare typically doesn't cover the costs of regular eye check-ups or expenses related to eyeglasses or contacts. Thankfully, there are several ways to reduce the costs of these necessities. Feel free to contact us and we can assist you in exploring all of your available options.

Learn what a Medicare broker does, why their advice is free and how they save you time and money. Discover how to find a trusted expert to guide you through your Medicare options—so you can make confident decisions about your healthcare coverage.