Medicare Coverage and Doctors (Part 1)

Senior citizens depend on Social Security and Medicare to meet their financial and medical needs. But now, there is concern among seniors that their doctors and clinics are going to stop accepting Medicare patients. In reality, most doctors accept Medicare patients. Often, a doctor who is not accepting a patient is doing so not because of Medicare but because their practice is full. Why are medical practices filling up with patients?

There is a concerning trend of medical students choosing to go into higher-paying specialties rather than general practice. They can earn almost twice as much per year as specialists. Because of this, as few as 3% of medical students choose family practice. As family doctors retire and fewer medical students choose to become family practitioners, a shortage of primary care physicians happens.

At the same time, a large number of Baby Boomers are reaching retirement age and Medicare eligibility. So, there is a shortage of doctors just as a large group of people becomes eligible for Medicare. In addition, Medicare reimburses doctors less than insurance companies for younger patients. A doctor can only see so many patients per day, so they try to balance non-Medicare and Medicare patients. A medical practice can only serve a certain number of patients.

Finding A Medicare Doctor

When a medical practice has reached the limit of patients they can handle, they will tell prospective patients they can not take new patients. The office staff might even say they are not taking Medicare patients when they should be saying they are not taking any new Medicare patients.

Congress must make changes to the Medicare program to address these problems so older patients continue to get the medical care they need. Medical students must be enticed to go into general medicine or family practice so the shortage of doctors is addressed. Medicare must reimburse doctors at a level similar to non-Medicare patient’s insurance. Since Medicare is paying out more than it brings in right now, funding solutions must be found to keep Medicare viable into the future.

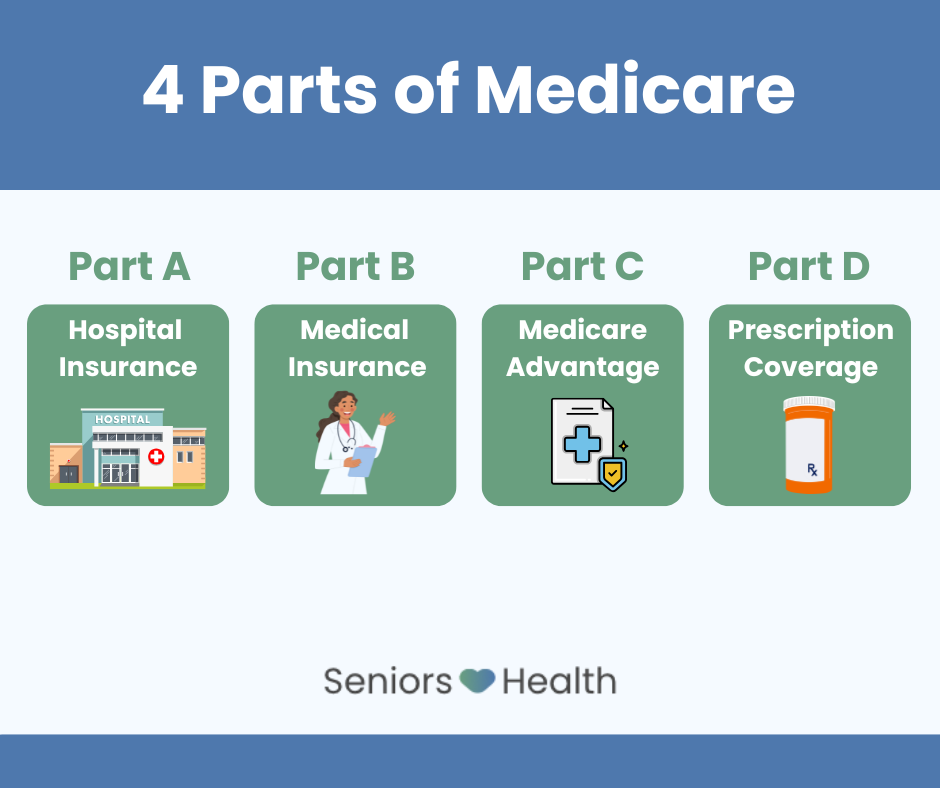

What is Medicare and the Medicare Network?

Medicare is a huge national health insurance network for senior citizens. This program is not limited to one area but covers all of the U.S. Many people are covered by some type of health insurance all of their lives. Many insurance programs are through a person’s employment, such as PPO plans. In addition to basic Medicare, many seniors opt to sign up for a Medicare Advantage plan with a secondary insurance company supplementing Medicare. Medicare plans have networks of doctors and hospitals their clients can use. Clients are required to contact the network before having medical treatment. Doctor’s offices often do this for patients.

The Kaiser Family Foundation, after studying recent surveys, has found that fewer than 3% of seniors had trouble finding a doctor when they needed one. This agency has found similar experiences when assisting clients in finding and getting appointments with their physicians. Most doctors accept some form of Medicare. We do research to find out which Medicare plans are accepted by most doctors. Most providers accept either Original Medicare or a Medicare Advantage plan network, or they accept both. Very few doctors fail to accept any form of Medicare.

Finding A Medicare Provider After You Move

Senior citizens often relocate after they retire. They might want to be closer to adult children, move to a warmer climate, or downsize to a senior community in a different part of the country. And, some seniors want to spend a few years on the road as RVers seeing America. After the couple is settled in their new mailing address, they must locate the medical professionals they need.

There may be a temporary problem accessing medical treatment until they call around and find new primary physicians and specialists in the Medicare network of providers. It is wise to look for medical providers before one is actually needed. Since there are record numbers of Baby Boomers joining Medicare every day, there is competition for primary care doctors to consider. Most doctors accept Medicare patients if they have room.

Since Medicare pays a lower rate of reimbursement than other insurance plans, medical practices might limit the percentage of Medicare patients they see. They must have non-Medicare patients as well as Medicare patients to keep their practices profitable. They will continue to see patients who reach retirement age and switch to a Medicare plan, but they must limit new patients on Medicare to make enough money to keep giving all their patients quality care.

Each Medicare patient will have a long list of Medicare providers in the form of a Medicare provider’s book or online. The senior citizen will need to find doctors accepting Medicare in their area and call them to see if they have Medicare patient openings. People who are working with good Medigap agents can ask them to help with locating a physician that accepts Medicare. Once a person has established themselves with the medical professionals in the new location, they are set.

I hope you enjoyed reading about Medicare Coverage and Medicare doctors. Please keep an eye out for Part 2 of this blog post, where I will go over finding doctors who accept Medicare.