What are the 4 Parts of Medicare?

Medicare is the federal health insurance program for people 65 and over, some younger with disabilities and those with End Stage Renal Disease. Medicare is a different program from Medicaid, which offers healthcare and services to those who meet the qualified lower income requirements. Anyone receiving Social Security Disability (SSDI) for 24 months, will also become eligible for Medicare.

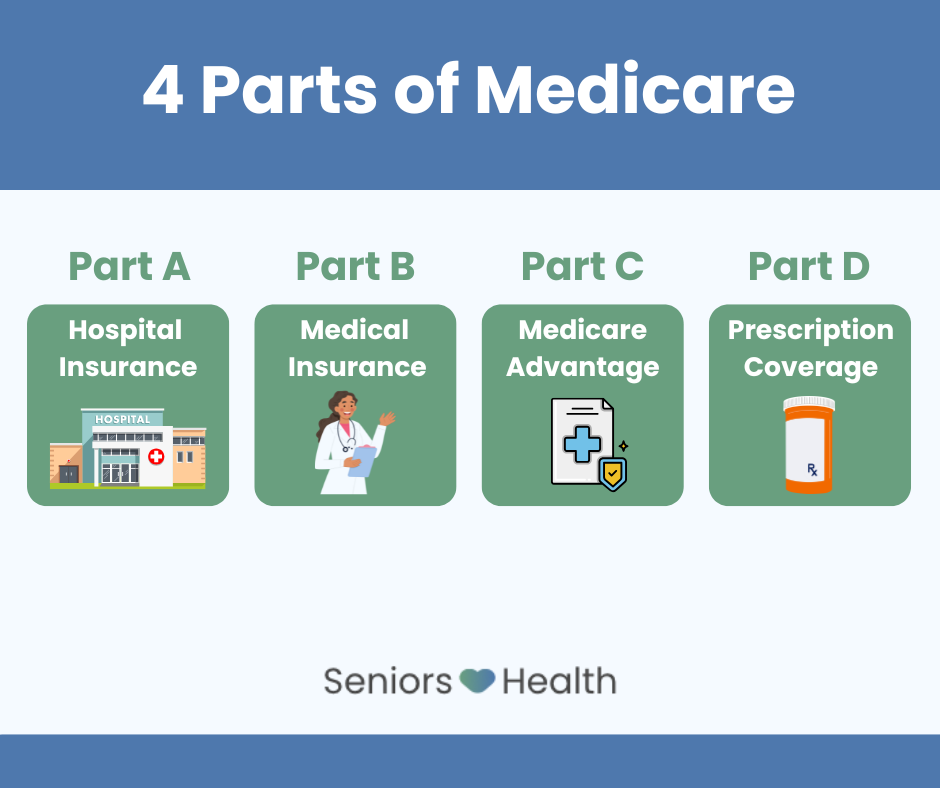

When discussing some of the Medicare basics, It’s important to know that there are 4 Parts of Medicare and each part works in a unique way to help cover your healthcare expenses.

What Is Medicare Part A and What Does It Cover?

Medicare Part A is inpatient and hospital insurance. Part A helps cover:

- Inpatient hospital care

- Skilled nursing facility care

- Hospice care

- Some home health care

What is Medicare Part B and What Does It Cover?

Medicare Part B is outpatient medical insurance. Part B helps cover:

- Services from a doctor

- Outpatient care

- Durable medical equipment

- Preventative services

- Some home health care

What Is Medicare Part C?

Medicare Part C (Medicare Advantage) are privately managed, federally approved Medicare plans.

Part C plans combine the benefits of Part A and B into one plan and may also include:

- Prescription drug coverage

- Dental, vision and hearing coverage

- Wellness programs and telehealth services

What Is Medicare Part D?

Medicare Part D plans provide beneficiaries with privately managed, federally approved prescription drug coverage.

Medicare Part A and B do not offer prescription drug coverage, so Part D helps:

- Manage prescription drug costs

- Provide lower cost-sharing for in-network and preferred pharmacies

What does Medicare Pay?

Medicare generally covers 80% of your Part A and Part B medical costs. You are responsible for the remaining 20%. There is no limit on what you pay out of pocket, unless you have Medicare Supplement coverage, also known as Medigap. You could also choose to get your coverage through a Medicare Advantage plan, also known as Part C. It is important to understand how each of these coverages work, when making a decision on how you would like to receive your benefits.

New to Medicare with Employer Coverage?

You should consider whether it makes sense to keep your employer coverage alongside Medicare or if switching to Medicare as your primary insurance would be a better option. A few key questions would include:

- How large or small is the employer?

- How much is your monthly premium?

- Would you like to have more freedom to choose any provider that accepts Medicare?

When it comes to Medicare, there is no one size fits all. Knowing your situation and what you find important, provides answers that help determine which road may be more suitable for you.

Avoid Costly Medicare Mistakes - Get Expert Advice

We understand that learning about Medicare can seem confusing. Especially knowing when and how to sign up for each part, to ensure you don’t miss any important deadlines. This is where our team of friendly agents can help. To learn which coverage options best suit your needs and how to avoid unexpected medical costs, contact us for a no-cost personalized review.